TDS Online Payment

How to Make TDS Online Payment: Know Details Here

TDS(Tax Deduction Source) is a process of subtracting the tax amount while making payments like interest, salary, commission, rent and so on. Usually, the person who is receiving income should be determined to pay income tax. However, the government is trying to deduct the tax in advance with the help and the provision of TDS payments. The salaried individuals are liable to pay the amount to the “Credit of the Central Government” through banks. The TDS amount deducted must be deposited to the government within the due dates specified by the person deducting the TDS. The TDS payment can be made online. The online payment gateway is offered by the NSDL to all the taxpayers for making the electronic payments of taxes using an internet banking facility from any bank.

What is TDS?

The full form of TDS is Tax Deducted at Source and a taxpayer must pay it if his income exceeds the specified limit. Any individual whose income exceeds a certain threshold is required to make TDS payment online or offline. The tax rates for TDS is prescribed by the tax department in India.

An individual or company that pays the TDS is called a deductor. And the individual or company that receives the payment is called the deductee. The deductor is responsible for the deduction of TDS before making any payment and deposit of the same with the India government. TDS is deducted on the following payments:

- Salaries

- Interest paid by the banks

- Rent payments

- Commissions payments

- Professional fees

- Consultation fees

What is TDS Return?

A TDS Return is a summary of all the transactions related to TDS made during a quarter. TDS Return is a quarterly statement submitted by the deductor to the Income Tax Department. After deducting TDS, the deductor has to deposit the same amount and its details to the government in a TDS return form.

Notably, different types of TDS forms are required to file different types of TDS deductions.

What is TDS Payment Due Date for Government Assesses?

Assesses connected with the Government will be required to make their TDS deposit before the following dates:

- Payment of TDS Tax without challan: on the day of deduction

- Payment of TDS Tax with challan: 7th of the succeeding month

What is TDS Payment Due Date for other Assesses?

The following are the TDS payment due dates for assesses who are not connected/ or are a part of the Government:

- The tax-deductible in the month of March till 30th April of the succeeding year.

- On 7th of the succeeding month for the deposit of tax by the employer.

How to make TDS Payment Online?

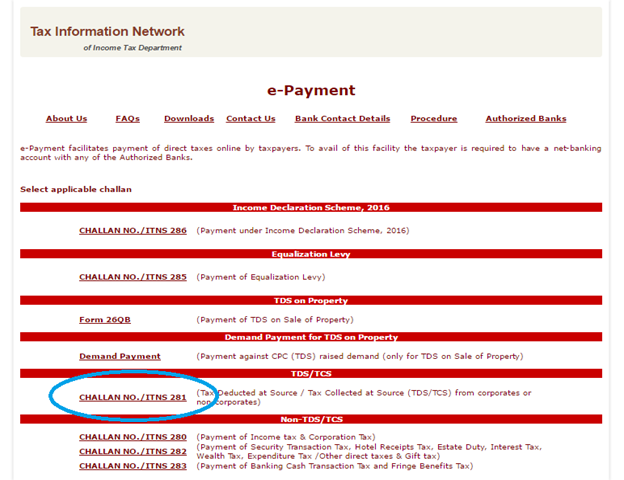

Step 1: Go to NSDL’s website for e-payment of taxes

Step 2: Select ‘CHALLAN NO./ITNS 281’ under TDS/TCS section. You will be directed to the e-payment page.

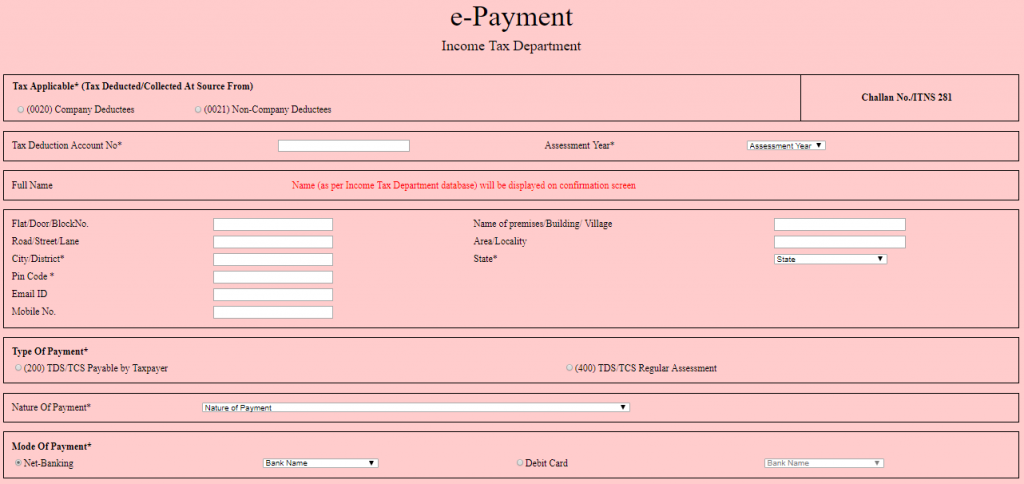

Step 3: In this page the following details have to be entered:

- Under ‘Tax Applicable’ select ‘Company Deductees’ if the TDS deducted by you is while making payment to a company. In any other case select ‘Non-Compay Deductees’.

- Enter the TAN and Assessment Year for which the payment is made.

- Enter the ‘Pin Code’ and select ‘State’ from the drop down.

- Select whether the payment is made for TDS deducted and payable by you or TDS on regular assessment.

- Select the ‘Nature of Payment’ and ‘Mode of Payment’ from the drop-down.

- Click on the ‘Submit’ button.

Step 4: On submission, a confirmation screen will be displayed. If TAN is valid, the full name of the taxpayer as per the master will be displayed on the confirmation screen.

Step 5: On confirmation of the data entered, you will be directed to the net banking site of your bank.

Step 6:The taxpayer should log in to the net banking site with the user id and password provided by the bank and make the payment.

Step 7: On successful payment, a challan counterfoil will be displayed containing CIN, payment details and bank name through which e-payment has been madeThis counterfoil is a proof of the payment made.

Note:After payment of TDS, you have to file your TDS return.

What are the Consequences of Delayed TDS?

Delay in TDS Payment

- If the deducted TDS is not deposited with concerned authorities by the given timeline, whether in whole or in part, as per Section 201(1A), the deductor is liable to pay an interest, applicable at a rate of 5% for every month or part thereof, from the date on which TDS was collected to the date on which such tax was actually remitted to the credit of the Government.

- Calendar month is considered in calculating interest and any fraction of a month is deemed to be a full month.

- Even a delay of one day would mean that you have to pay interest for two months.

- In case TDS is deducted in the month of July and deposited on 8th of August then you have to pay interest for 2 month i.e. July and August. Total interest payable shall be 3%.

In addition to the interest clause applicable, there are additional provisions for penalty and prosecution proceedings as well.

Penalty under Section 221

- In case the Assessing Officer is convinced that the assessee has failed to deduct tax as required, without any good and adequate reason, the defaulter is liable to imposition of penalty.

- The quantum of penalty is not to exceed the amount of tax in arrears.

Penalty under Section 271C

- A penalty equal to the amount of tax that the deductor has failed to deduct can be imposed.

- However, such penalty can be levied only by a Joint Commissioner of Income Tax.

Prosecution proceedings under Section 276 B

- Where the deductor has failed to deposit the tax deducted at source, with the concerned government authorities, without a reasonable cause

- He/she is liable to be punished with rigorous imprisonment for not less than 3 months to 7 years and with fine.

Delay in TDS Deduction

- TDS needs to be deducted by the 30th of each month and in the month of February, it should be deducted by the last day of the month.

- If the TDS is not deducted on the required due date, whether in whole or in part, then the concerned deductor is liable to pay interest, applicable at a rate of 1% per month or part thereof, from the date when it should have been deducted to the actual date of deduction.

Delay in TDS Return Filing

- As per Section 234E, in case an assessee fails to submit the TDS return within the specified due dates, they will be liable to a penalty of Rs.200 per day till the time the TDS return is actually submitted.

- The penalty amount cannot exceed the total amount of TDS collected.

- This penalty is also applicable in case of furnishing Form 26 QB, in case of purchase of immovable property.

Note: Delay in filing of TDS returns for more than a year from the due date or submission with incorrect data such as TAN, Challan Number, TDS Amount etc. will attract a minimum penalty of Rs.10,000 and not be more than Rs.1,00,000.

How to Check TDS Payment Status?

Assessees can check the TDS payment status online through the online portal of Centralized Processing Cell. Here’s how to do it :

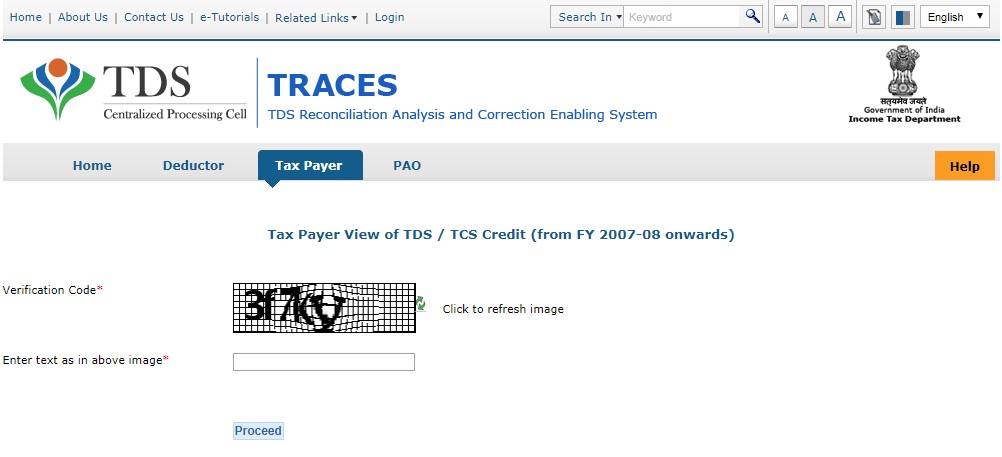

Step 1: Visit TDS CPC website (https://www.tdscpc.gov.in/app/tapn/tdstcscredit.xhtml)

Step 2: Enter the captcha code and click on “Proceed”

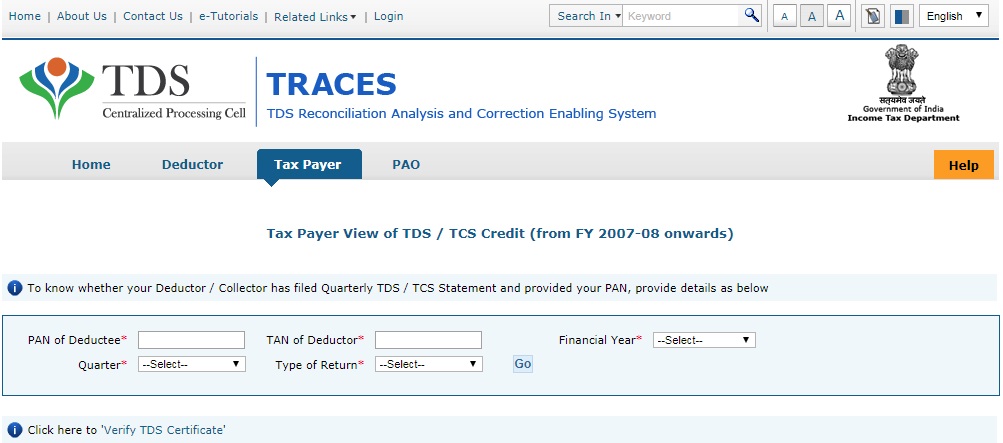

Step 3: Enter details such as PAN of deductee, TAN of deductor, Financial Year, Quarter and Type of Return. Click on “Go” now.

Step 4: TDS credit of the taxpayer is displayed on the screen

TDS Certificate

TDS certificate, Form16 and Form 16 A issued on an annual or quarterly basis. After making TDS payment with the Income Tax Department, as per the provision of Section 203, the deductor is required to provide a TDS certificate to the person on behalf of whom tax payment was being made.

TDS Due Dates

| Deduction Month | Quarter end date | TDS Payment Due Date | Due date for filing returns |

| April | 30th June | 7th May | 31st July |

| May | 30th June | 7th June | 31st July |

| June | 30th June | 7th July | 31st July |

| July | 30th September | 7th August | 31st October |

| August | 30th September | 7th September | 31st October |

| September | 30th September | 7th October | 31st October |

| October | 31st December | 7th November | 31st January |

| November | 31st December | 7th December | 31st January |

| December | 31st December | 7th January | 31st January |

| January | 31st March | 7th February | 31st May |

| February | 31st March | 7th March | 31st May |

| March | 31st March | 7th April | 31st May |

TDS Filing or TDS Returns Forms

TDS return needs to be filed by the person, organization or institutions, who have deducted tax, on a quarterly basis. As per section 201(1A), interest for delay in the payment of TDS should be paid before filing the TDS return.

There are several forms, based on the nature of deduction:

- Form 24Q: To be filled out for all the deductions made from salaries

- Form 26Q: To be filled out for all the deductions made from payments other than salaries

- Form 27Q: It is the TDS quarterly return to be filled out by the deductor for all deductions made in case of NRIs

- Form 27EQ: It is the TCS quarterly return to be filled out by the deductor

- Form 27A: This form has to be signed and accompanied by quarterly statements

Note: The TDS returns need to be filed on a quarterly basis and the due date for the same is 31st of the month after the end of the concerned quarter.

What are the Benefits of TDS Online Payment?

- Availability of 24*7 Payment facility on all 365 days of the year

- Convenience in terms of time and place for the deductor to make the TDS payment as convenient

- TDS Online Payment acknowledgement on immediate basis

- Facility to download the challan acknowledgement copies and save them easily for reference in the future

- Significant decrease in the chances of corruption and other malpractices like the discretionary grant credit of tax deductions based on manual TDS Certificates etc. due to a secure, transparent system online

- Also, e-filing TDS makes it environment friendly due to the saving of paper to a great extent and in great quantity