How to View Filed TDS Statement Online?

Employers and organisations that deduct tax at source can check the TDS statement after filing the statement, just to make sure everything is correct. You simply need to visit the IncomeTax efiling website and follow a few simple steps to view the filed TDS statement online.

Step 1: Visit the income tax e-filing portal at the URL. ( http://www.incometaxindiaefiling.gov.in/home)

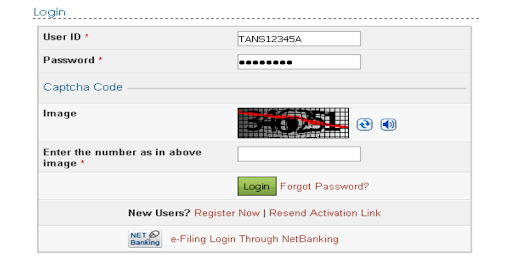

Step 2: Log in to the e-filing portal with your log in credentials.

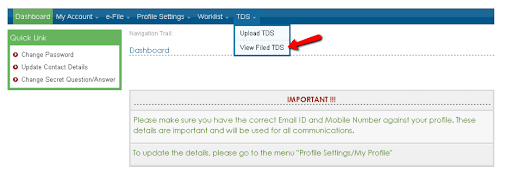

Step 3: Select the ‘View Filed TDS’ option under the ‘TDS’ tab.

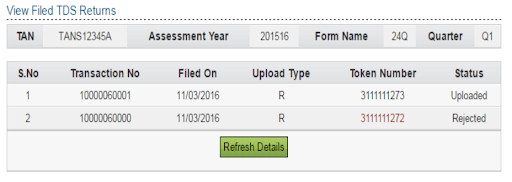

Step 4: Select the financial year, form name, and quarter, from the dropdown menu for which the TDS statement was uploaded. Click on the ‘View Details’ button.

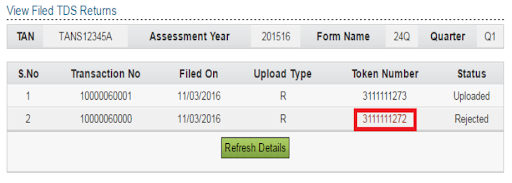

Step 5: The details of the TDS statement will be displayed. Once you upload the TDS statement, the ‘Status’ column will be shown as ‘Uploaded’. Upon validation, the status will either be ‘Accepted’ or ‘Rejected’.

The final judgement will be reflected on the portal within a period of 24 hours from the time of upload.

Step 6: If the statement is rejected, it will state the reasons for rejecting it. Click on the token number to view the rejection reasons.

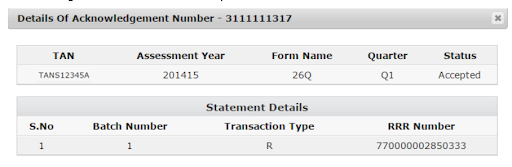

Step 7: If the status is ‘Accepted’, click on the token number to view the acknowledgement details of the uploaded TDS statement.

Follow these steps above and check your filed TDS statement anytime.

Frequently Asked Questions (FAQs)

Q.Who is required to file e-TDS/TCS return?

A.As per Income Tax Act, 1961, all corporate and government deductors/ collectors are compulsorily required to file their TDS/TCS returns on electronic media (i.e. e-TDS/TCS returns). However, deductors/collectors other than corporate/government can file either in physical or in electronic form.

Q. e-TDS/TCS returns have been made mandatory for Government deductors. How do I know whether I am a Government deductor or not?

A.All Drawing and Disbursing Officers of Central and State Governments come under the category of Government deductors.

Q. Under what provision should e-TDS/TCS returns be filed?

A.An e-TDS return should be filed under Section 206 of the Income Tax Act in accordance with the scheme dated August 26, 2003 for electronic filing of TDS returns notified by the Central Board of Direct Taxes (CBDT) for this purpose. CBDT Circular No. 8 dated September 19, 2003 may also be referred.

An e-TCS return should be filed under Section 206C of the Income Tax Act in accordance with the scheme dated March 30, 2005 for electronic filing of TCS returns notified by the CBDT for this purpose.

As per section 200(3)/206C, as amended by Finance Act 2005, deductors/ collectors are required to file quarterly TDS/TCS statements from FY 2005- 06 onwards.

Q.Who is the e-Filing Administrator?

A.CBDT has appointed the Director General of Income Tax (Systems) as e-Filing Administrator for the purpose of electronic filing of TDS/TCS returns.

Q.Who is an e-TDS/TCS Intermediary?

A.CBDT has appointed National Securities Depository Limited, (NSDL), Mumbai, as e-TDS/TCS Intermediary. NSDL has established TIN Facilitation Centres (TIN-FCs) across the country to facilitate deductors/ collectors filing their e-TDS/TCS returns.

Q. Is there any software available for preparation of e-TDS/TCS return?

A.NSDL has made available a freely downloadable return preparation utility for preparation of e-TDS/TCS returns. Additionally, you can develop your own software for this purpose or you may acquire software from various third party vendors. A list of vendors, who have informed NSDL that they have developed software for preparing e-TDS/TCS returns, is available on the NSDL-TIN website.

Q.Are the forms used for e-TDS/TCS return same as for physical returns?

A.Forms for filing TDS/TCS returns were notified by CBDT. These forms are the same for electronic and physical returns. However, e-TDS/TCS return is to be prepared as a clean text ASCII file in accordance with the specified data structure (file format) prescribed by ITD.